Are central banks afraid ?

By Alexandre Hezez, Group Strategist

Editorial

Being late in the normalization of interest rates, central banks had to and were able to accelerate the pace at an historical level. Starting the end of 2021 and for months, the Federal Reserve constantly repeated that the price increase was transitory, partly due to supply issues and components shortages. Then, Jerome Powell estimated before the Senate Banking Committee that “ the time has probably come to stop using the word transitional “and that ” the risks of more persistent inflation have increased “. This was in contrast to the official position of his European counterpart. However, the war in Ukraine has changed this fragile situation and maintained a movement that was already well established.

Sources : Bloomberg, Richelieu Group

Western central banks lagged behind in the face of rising prices, but they quickly became real inflation fighters, as evidenced by the overall interventions.

The purpose of a central bank is to maintain the economic and financial stability of the country by controlling the money supply and influencing interest rates. The initial causes of the return of inflation are well known. They have emerged post-pandemic with the disruption of supply chains and investment plans promoting environmental transition. Then, the war in Ukraine disrupted the balance of commodity prices, especially energy prices. This chain of events then indirectly affected the prices of manufactured goods and services, making inflation a broader and potentially persistent problem.

Paradoxically, for almost 10 years, monetary policies were focused on fighting the risk of deflation, sovereign risk and the proper transmission of the banking system to the economy. However, now that inflation has become a major concern, central banks are returning to their original mandate : to fight against inflation and to maintain economic stability.

Managing inflation expectations has become paramount to the detriment of steering monetary aggregates. These expectations, issued by the financial markets or economic actors, are crucial to guide decisions on prices and wages in the future, and thus determine the level of interest rates. The credibility of central banks is thus fundamental. This must be reflected in their communication as well as in their actions.

Their independence, unwavering determination and ability to act to bring inflation down to 2% are many of the variables in the equation. Credibility requires strong rhetoric and adequate communication to avoid over-interpretation by markets that would counteract the effects of monetary policy. Indeed, let’s take the case where inflation starts to fall and communication becomes more accommodating. Such a scenario would fuel expectations of monetary loosening and improved credit conditions… The latter would again become inflationary and provoke a deeper crisis requiring more brutal action to contain it.

The essential tool, the “forward guidance” , used by central banks, was already abandoned last year in view of the uncertain context. We are navigating in the mirror situation, where the monetary authorities have to create uncertainty to avoid any anticipation and prognosis from the markets and maintain a risk premium over time. The balance is precarious: avoiding excessive volatility or even a crisis and stemming any hard-to-manage recovery in inflation. In short, the low visibility granted by central banks must be compensated by firm and transparent communication.

Keeping medium-term inflation expectations anchored near the inflation target remains crucial to avoid any self-fulfilling change in economic agents. For now, the battle is won but the fight is far from over.

Sources: Bloomberg, Richelieu Group

Are central banks looking for a recession ?

In August 2022, Jerome Powell’s speech at the Jackson Hole central bankers’ conference emphasized his frank intention to use ” vigorously all its tools ” and ” a long period of lower growth “ thus ” that a slowdown in the labor market ” before concluding ” the fight against inflation in the United States will hurt U.S. households and businesses but giving it up would be even more damaging to the economy “.

The stated objective for the coming months is to prevent demand from accelerating faster than supply. So once again, we have to restrict the financing conditions. Disinflation will be long and laborious. Of course, we already have inflection points, but they are still very far from the desired standards.

Recent figures in the United States and Europe suggest a more complex situation. Financial conditions have largely eased and consumption remains strong (linked to a very robust labor market and the use of Covid savings). The Fed was faced with a nasty surprise regarding inflation with the release of the PCE data that far exceeded expectations to the upside. After several months of slowdown, inflationary pressures picked up again in January, both in annual and monthly variation, for total inflation (+5.4% year-on-year vs. +5.3% in December) and core inflation (+4.7% vs. +4.6%). This revision, significantly higher than historical, also raised concerns, confirming that the Fed still has a lot of work to do. FED members are now facing increasing pressure as the PCE index is their preferred indicator for inflation analysis. The central bank will focus on the services component excluding housing, which continues to accelerate strongly in January as business leaders pass on past wage increases to prices (this is even the third month of acceleration). The risks of second-round effects are materializing, which is the main point of vigilance when the next indicators are published and the March 22 meeting is held. Some members spoke out after the inflation numbers were released, talking about the need to raise rates several times, without committing to a clear terminal rate, or the need to go back to 50 bp steps.

Source : Twitter @NickTimiraos

Despite the strength of inflation, the loss of household purchasing power remains moderate and households continue to consume, as evidenced by the increase in January in consumer spending in value and volume terms, while the savings rate has risen slightly. The slowdown in prices and growth expected by the Fed remains far too moderate to allow it to consider the end of monetary tightening, which leads us to revise upwards our key rate and short rate targets. We remain cautious about the terminal rate level that will need to be achieved (financial investors’ expectations are now at 5.4% according to future curves), even if we should not underestimate the future spread of the effects of the extent of the monetary tightening that has already taken place, particularly in real estate.

In Europe, with a bit of a delay, the situation is similar. The inflation rate in the Eurozone has fallen, with the consumer price index at 8.6% in January from its peak of 10.6% in October. However, core inflation, which excludes changes in energy and food prices, continues to rise and reached a record high of 5.3 percent in January. The markets, fearing persistent inflation, have revised upwards the expected levels of terminal policy rates.

The markets were expecting a rapid cut in Fed policy rates as early as the second half of the year, but that prospect has been pushed back to 2024. As a result, policy rates will remain higher for an extended period.

What can central banks be afraid of?

Like Ben Bernanke, chairman of the FED from 2006 to 2014, who constantly referred to the Japanese deflation of the 1990s, Jerome Powell bases his analysis on the last stagflation episode of the 1970s. According to him, the mistake the FED made in the 1970s was to fear plunging the economy into a sharp recession and then quickly lowering interest rates. Jerome Powell prefers to be considered as a second Paul Volcker rather than a second Arthur Burns (Fed Chairman from 1970 to 1978). It was not until 1975, far too late, that Burns admitted that the United States had an inflation problem. The lesson of this whole episode is painful: it is very dangerous to ignore transitory factors. At the time, when Carter appointed Volcker as head of the Fed in July 1979, he decided to reverse U.S. monetary policy. So the question is whether Jerome Powell has an unlimited capacity to normalize the situation. The United States experienced high inflation in the 1970s and into the early 1980s.

Source : https://www.bis.org/review/r021126d.pdf

We would almost have liked to find a paper of this scope written by Jerome Powell to clarify his thoughts !

The inflationary crisis of 2022 is a direct consequence of the 2020 Covid crisis, which led to supply chain and labor disruptions, “stop-and-go” on the demand side (amplified by a shift from services to goods), as well as massive monetary and fiscal stimulus. The outbreak of armed conflict in Europe and the escalation of Sino-American strategic tensions have only exacerbated the upward pressure on prices. Almost naturally, a disinflationary feedback effect has been set up on the basis of the factors we have already explained.

However, the decline in inflation and interest rates will strengthen real household income in an environment of already healthy consumer finances, strong corporate balance sheets and less leveraged banks. Demand should then increase, which could fuel a new wave of inflation. Inflationary pressures rarely stay on a high plateau, they rather tend to come in waves. The fear of the central banks is that they are on an inflationary ridge whose second wave would be more difficult to control, which projects them into the scenario of the 1970s.

The initial causes of this return of inflation are well known, and mainly external: disruptions of global supply chains after the pandemic, energy prices, war in Ukraine… The indirect impact of these changes was gradually passed on, first to the prices of manufactured goods and then to the prices of services. To summarize, inflation has become not only higher but broader ; not only imported but domestic ; not only linked to a temporary supply shock but potentially persistent. Therefore, no one can seriously deny that monetary policy must react. So back to the original mandate… the fight against inflation.

The important questions now are the extent, speed and duration of this monetary policy tightening to avoid this scenario. Financial markets, through their strength, and governments, through their support plans, can potentially counteract monetary actions. ” Financial investors may be underestimating the persistence of inflation in the Eurozone “This is a good thing,” said Isabel Schnabel, a member of the European Central Bank’s Governing Council, in a speech. Controlling inflation will not only require a balance between central banks, governments and financial markets. The money supply is rapidly shrinking and this is a declared will that must have an effect in the long run.

Sources: Bloomberg, Richelieu Group

But beyond monetary policy considerations, the real question that should perhaps be asked lies in the ability of central banks to control intrinsic trends in price dynamics . For now, we need to create uncertainty about the possible aggressiveness of monetary actions: ” our future decisions will remain data-dependent and will continue to be made on a meeting-by-meeting basis ” to avoid any anticipation. Lowering demand, managing credit conditions, monitoring real rates are certainly necessary conditions, but they are not sufficient. There is a kind of unsolved mystery in price dynamics that central banks do not master. The behavior of economic agents is not necessarily rational and does not match economic equations. During the 2009-2018 (or even 2020) period, price dynamics have been amorphous even though central banks have been continuously implementing money creation. Wouldn’t it be possible to consider, this time, an antithetical situation…

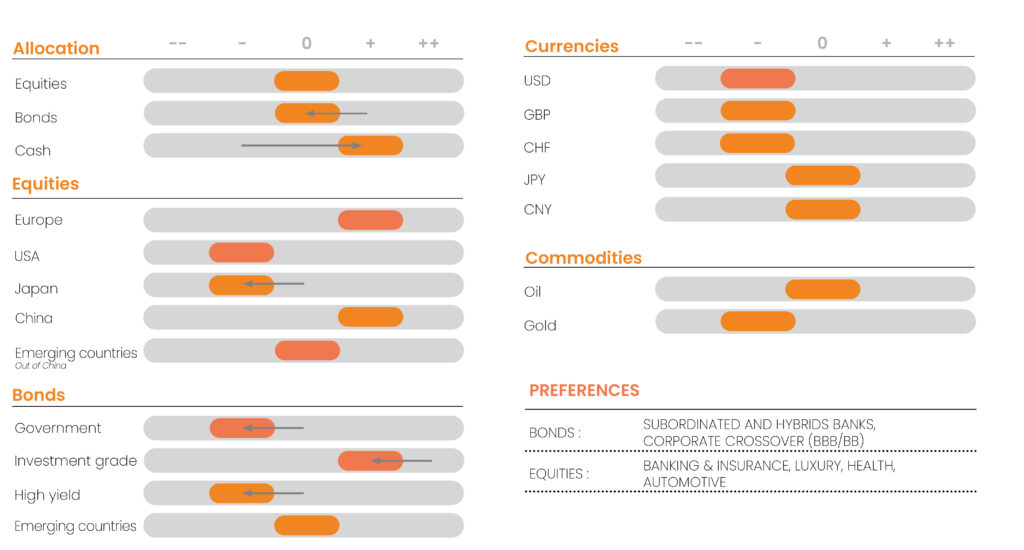

CONVICTIONS

POSITIONING WITH RESPECT TO RISK CRITERIA

Don’t take risks with inflation : Short-term prudence in the face of inflationary doubts

According to industry and household surveys, there is still a high risk of recession, confirmed by bond market curves that show a reversal of the yield curve. Such an inversion of the yield curve normally reflects expectations of a deterioration in activity and inflation, to the extent that it implies the end of a tightening cycle and a rapid reduction in interest rates by central banks.

We believe that the context, both historical and academic, is very different. It reflects not only the strong commitment of the monetary authorities to fight inflation, but also their credibility in doing so.

Sources : Bloomberg & Richelieu Gestion

Recent real activity indicators show economies holding up well, despite high inflation and refinancing rates and the recent energy crisis. Labor markets are showing strong momentum, with employment levels well above pre-Covid levels.

Sources : Bloomberg & Richelieu Gestion

The rebound of the equity markets also sends a signal of improvement in macroeconomic expectations (reopening of China, employment, consumption) and micro-economic expectations at the corporate level (rather reassuring results and outlook). The tightening of monetary policy already in place will begin to dampen activity. Central banks have already significantly tightened their monetary policy either by raising key rates or by reducing their balance sheets. The recent release of inflation figures has reminded investors that the fight is far from over. Central banks, as a whole, will have to continue to “scare” the market to avoid any inflationary improvement in credit conditions. Dynamic labor markets encourage wage growth, which propagates price pressures. Central banks will finalize their rate hike cycle in the first part of the year before pausing to assess the effects of their policies. While headline inflation will continue to decline in 2023, core inflation pressures will persist and encourage central banks to remain vigilant and aggressive in their rhetoric. However, they will not lower their rates in 2023 or well into 2024. Even if we accept that policy rates are close to their maximum, it is unlikely that the central bank will want to take risks with inflation, especially if labor markets remain buoyant.

We continue to favor a soft landing scenario. We remain confident that the economies will be able to avoid a recession. Indeed, strong labor markets and lower inflation will be real supports for households. Covid savings” are still available as a shock absorber and have yet to deliver their consumption capacity in China. Continued tight monetary conditions should limit overly vigorous growth, which is harmful to financial markets. The rate hikes that have already taken place have brought activity in most real estate markets to a halt and are weighing on the financing capacity of businesses.

Sources : Bloomberg & Richelieu Gestion

In terms of equity allocation, given the latest figures released, the coming weeks are likely to crystallize fears about the attitude of central banks to a surprisingly resilient labor market.

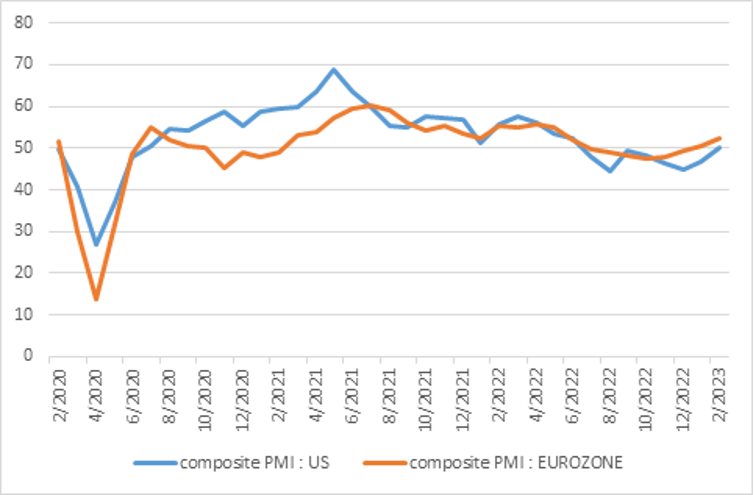

Eurozone and US PMIs continued to rebound in February, hitting four-month highs thanks to lower energy prices in Europe and improved consumer purchasing power as inflation eased. The PMI increase adds fuel to the fire ignited by the strong US employment numbers and retail sales. These statistics imply permanently higher interest rates. Monetary tightening affects growth with about a 10-month lag. With the Fed having begun its rate hike cycle 11 months ago, the effects will begin to be felt in the economy (tightening credit conditions, deteriorating credit flows, slowing money supply growth).

Sources: FED, BofA

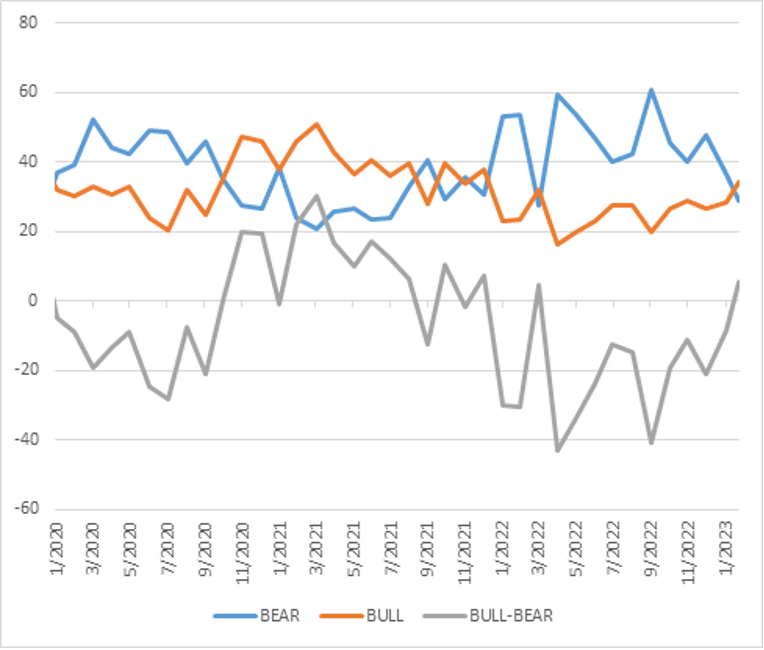

Even if we are convinced that the monetary effects will have the expected impact on the year, we should have a correction phase to take advantage of. Investor sentiment has returned to an optimistic zone (as shown by the Bull-Bear indicator) marking a zone of volatility in the face of uncertainties.

Sources: FED, BofA

We are again maintaining our overexposure to the European equity market, which continues to benefit from valuation differentials and favorable macroeconomic elements. The proven easing of the energy crisis and the resilience of the European economies lead us to favour this market as it appears particularly attractive in terms of valuation Moreover, its sector composition (more value, more dividends) is less sensitive to higher rates. The small and mid cap segment could benefit from this craze in the coming months, helped by a catch-up effect and historically very low valuations compared to large caps.

China’s reopening remains favorable to the local market as well as those of its trading partners. Continued tensions between China and the United States could create favorable entry points in the coming weeks.

Sources: Bloomberg, Richelieu Group

Regarding Japan, we are downgrading our view to focus on emerging asian countries. The change of governor at the BoJ (Bank of Japan) creates a lot of uncertainty. The accommodative policy will be difficult to maintain given the impact on the currency. The next steps should be taken in order to support the Yen. Salaries are still struggling for the time being. This is the main reason for the deteriorating market outlook. Japanese companies, many of which depend on exports, are particularly benefiting from an improving situation in China, which will pick up in the second half of the year.

We still underweight on the US segments, as the US central bank could show that it can go much further and make investors fear stronger action at its next meeting. Growth stocks, which have outperformed significantly since the beginning of the year, could suffer from the pressure on valuations. The flows of the last 3 years have been concentrated on this geographical area and should still undergo some arbitration in the months to come. Some themes seem interesting to us: dividend growth, relocation and digitalization.

In the short term, we are also downgrading bond investments to neutral in order to reposition ourselves more strongly once the housing and services sector will mark a decline in terms of inflation (particularly on the sovereign parts but also corporate credit on the long parts). The interest rate markets are beginning to integrate a new acceleration of the economy and could lead the FED and the ECB to take more action against inflation. Spread decreases should moderate, or even reverse in the short term. The riskiest segments should suffer in these conditions. We remain positioned in the BBB-/BB segment, which we believe to be the most resilient (with a preference for the Euro segment).

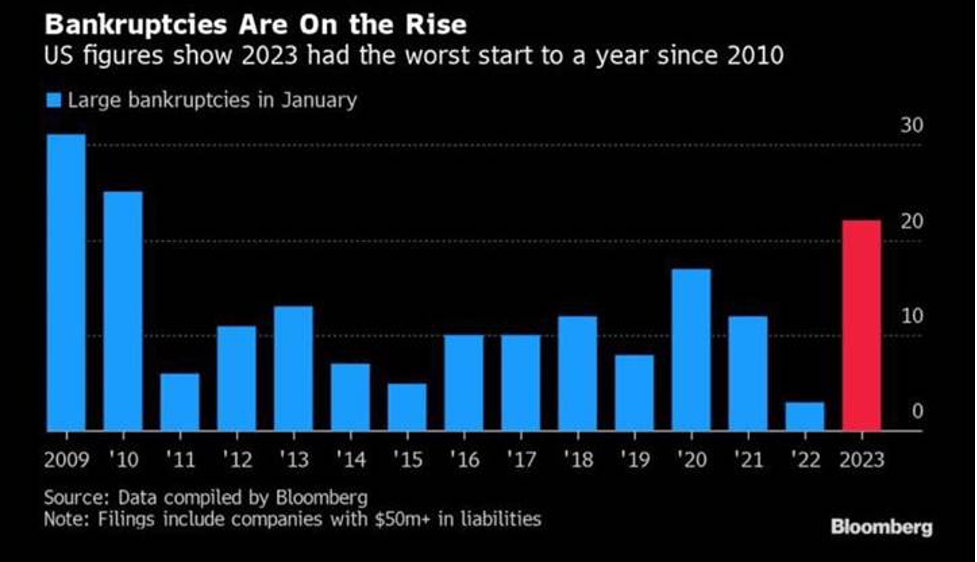

The number of bankruptcies is increasing in the United States. This phenomenon is largely linked to the deterioration of credit conditions for the most vulnerable companies in terms of their balance sheets.

The higher interest rate environment encourages us to maintain our exposure to highly rated corporate debt. In the short term, doubts about inflation and the attitude of central banks wanting to maintain their credibility at all costs in defending price stability are leading us to temporarily increase the levels of cash in portfolios. Credit spreads have narrowed far too quickly for our liking and without real discernment. Selectivity will be the order of the day.

Sources: Bloomberg, Richelieu Group

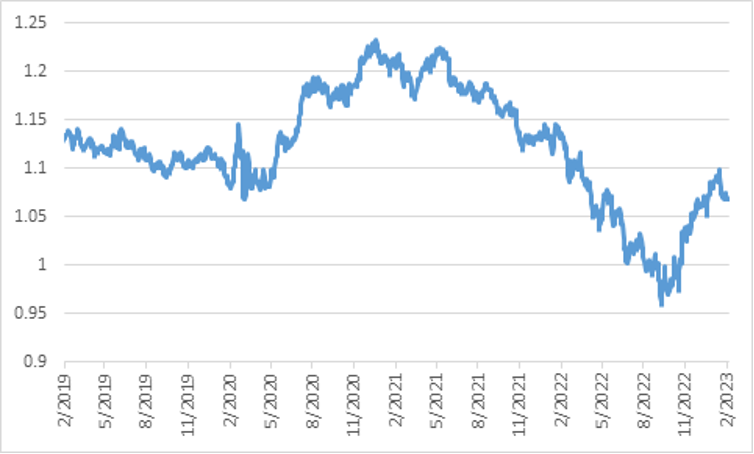

Regarding the euro/dollar exchange rate : the rate differential anticipated by the markets and the concerns about the European economic outlook in 2022 had largely contributed to the fall of the euro, before fading and allowing the single currency to recover. These two factors were previously well integrated into prices, but the persistence of US inflation, a higher than expected FED terminal rate and especially the resurgence of geopolitical tensions between China and the US has allowed the dollar to regain strength. We believe that the Fed remains ahead of the cycle and that the euro should continue to strengthen in 2023, starting with the next ECB monetary policy meetings.

Sources : Bloomberg, Richelieu Group

Synthesis Strategy Richelieu Group – Author

Disclaimer

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

The information, opinions and estimates contained in this document are for information purposes only. No element can be considered as an investment advice or a recommendation, a canvassing, a solicitation, an invitation or an offer to sell or to subscribe to the securities or financial instruments mentioned. The information provided concerning the performance of a security or financial instrument always refers to the past. Past performance of securities or financial instruments is not a reliable indicator of future performance.

All potential investors should conduct their own analysis of the legal, tax, accounting and regulatory aspects of each transaction, if necessary with the advice of their usual advisors, in order to be able to determine the benefits and risks of the transaction and its appropriateness to their particular financial situation. He does not rely on Richelieu Gestion for this.

Finally, the content of the research or analysis documents or their excerpts, if any, attached or quoted, may have been altered, modified or summarized. This document has not been prepared in accordance with the regulatory provisions designed to promote the independence of financial analysis. Richelieu Gestion is not prohibited from trading in the securities or financial instruments mentioned in this document prior to its publication.

Market data is from Bloomberg sources.